Quarterly Letter — Q1 2023

Dear Owner Partner -

You might not think a book about the long-lost craft of making wooden wagon wheels with hand tools in late 19th century England would be interesting to read or have anything to do with investing, but I do.

After reading about the English master wheelwright, George Sturt, in All Things Shining: Reading the Western Classics to Find Meaning in a Secular Age by Hubert Dreyfus and Sean Dorrance Kelly, I read his incredible book, The Wheelwright’s Shop. It provides deep and dramatic autobiographical insight into when craftsmen’s skills were primary to how people economically organized their life. Sturt was the last of several generations of true wooden wheelwright artisans that went extinct after the widespread introduction of more advanced technology, such as combustible engines and rubber tires, became a thing.

Today we think of “skill” as some practical capability in something worthwhile. However, the wheelwrights’ mastery went well beyond that. Like those before them, craftsmen learned their individual skills from their masters through a very long and thorough apprentice program. After becoming a true master of the wheelwright craft, he had an intimate understanding of the differences in the quality of wood that is not easily or quickly learned. It took a long time and many reps. In Sturt’s words:

“The skilled workman was the final judge. Under the plane (it is little used now) or the axe (it is all but obsolete) timber disclosed qualities hardly to be found otherwise. My own eyes know because my own hands have felt, but I cannot teach an outsider, the difference between ash that is “tough as whipcord,” and ash that is “frow as a carrot,” or “doaty,” or “biscuity.” In oak, in beech, these differences are equally plain, yet only to those who have been initiated by practical work.”

An expert wheelwright understood that every piece of wood he encountered had its own “personality” and “individuality.” Sturt believed that to be a true master of wood, you needed to know precisely how to approach the wood with the tools at hand. The wood is never a “helpless victim” against the tools but would “lend its own subtle virtues” to the wheelwright who “knew how to humor it: with him, as with an understanding friend, it would cooperate.” When working with unique pieces of wood, intelligence and flexibility are continuously required rather than thoughtless repetitive action.

Taking all of that a step further, Sturt believed the chief task of the craftsman was not to generate or create meaning - in this case, the final crafted product - from the wood. That is for the aesthetic pursuit of artists without regard for the longevity of a well-designed and well-built wagon wheel. Instead, he believed the master craftsman cultivated in himself the skill for discerning the meanings in the wood that were already there that lent themselves to good design and long-term durability. These meanings are hidden from the untrained wheelwright.

At North Beach, we think of ourselves as craftspeople of sorts. We organize our economic lives by working toward mastery as operating craftspeople, culture craftspeople, and capital allocation craftspeople.

About the latter, throughout our aggregate career, we have studied, analyzed, and considered countless opportunities to buy ownership stakes in private and public companies. That is, we got our reps in and will continue to do so. However, like a master wheelwright, we cannot create actual, intrinsic value in a company we buy if it is not there. We are not artists.

We work toward mastery of two skills to discern the value of a company already there.

First, like Sturt finding the correct type of wood for, say, a wagon spoke (in this case, he uses oak), we work to find the prized attributes in an essential service company’s business model that lend themselves to how we discern value. These attributes include recurring revenue (the company’s customers come back to purchase the service again and again), high “switching costs” (for whatever reason, it is expensive to move to another service provider), and acyclicality (the company is enduringly profitable no matter the macroeconomic climate). Sturt says one could use ash for spokes, but they will not last as long as oak. Similarly, if the attributes we seek are not there, our long-term value may not be realized.

Then, similar to Sturt’s guidance on finding the right piece of the correct type of wood for a spoke (oak sapwood for the front of the spoke because it takes paint better, and on the back, where you need strength, oak heartwood is used), we have to pay the right price for company ownership to realize value. For example, the wheel’s strength can be compromised if a wheelwright uses oak sapwood for the back. Similarly, if we overpay for a company, our return on our sacred capital will be compromised or permanently lost in a worst-case scenario.

Sturt provided learned guidance on the continuing work from apprenticeship towards mastery:

“There was nothing for it but practice and experience of every difficulty. Reasoned science for us did not exist. Theirs not to reason why. What we had to do was to live up to the local wisdom of our kind; to follow the customs, and work to the measurements, which had been tested and corrected long before our time in every village shop all across the country. A wheelwright’s brain had to fit itself to this by dint of growing into it, just as his back had to fit itself into the suppleness needed on the saw-pit, or his hands into the movements that would plane a felloe [the outer rim of a wheel where the spokes are fixed] ‘true out o’ wind’…He felt it, in his bones. It was a perception with him. But there was not science in it; no reasoning. Every detail stood by itself, and had to be learnt either by trial and error or by tradition.”

More directly, Sturt’s grandfather, a wheelwright himself, was fond of saying, “Nobody could learn to make a wheel without chopping his knee half-a-dozen times.”

In our craft, we have the knee scars to prove it, saying nothing about the wagon wheels we have made that have collapsed from making “type of wood” and “piece of wood” mistakes over the years. Of course, we think we learned from our past mistakes, but with humility, we know we will make more mistakes in the future.

As operating, culture, and capital allocation craftspeople, we spend time crafting what we can control. We don’t attempt to craft the stuff out of our control, like macroeconomics, the fallout from runs on crappy banks (BTW, we keep our bank checking account balances below $250,000 and invest the rest directly in U.S. Treasury bills), or the volatile price of commodities. The future outcomes of those things are important but unknowable. We are not macroeconomic pundits, don’t invest in financial service companies, and are not commodity strategists. We don’t focus on predicting the direction of inflation or interest rates or when we will be in a recession. We don’t need to worry about the net interest margin compression of the banking sector. We know we cannot predict where the price of tradable but not investable commodities will be. Each of these pursuits is a waste of our time.

For us, it is more beneficial to try and understand what is happening now in the areas we can craft. We are business analysts and operators and stay within our tight circle of competence. We focus on finding outstanding small private and public service companies at sensible prices - not mediocre companies at bargain prices. We work hard to understand them deeply from the bottom up and allocate capital accordingly. We then strive to operate our owned private companies well and be an excellent partner to our owned public companies. All the while, we are looking to build an incredible culture.

Our path forward endures: acquire, operate, and partner with attractively priced, well-run small private and public service companies that can deliver free cash flow growth for a long, long time. There is no fundamental difference between owning an exceptional private operating company and owning the common stock of an exceptional public company. We protect, enhance, and deploy our hard-earned and sacred permanent capital in a durable, concentrated, and differentiated collection of superior service companies. These companies are run by able and honorable entrepreneurs with important and unique long-term competitive advantages, so free cash flow earnings will likely be materially higher many years from now.

HOLDING COMPANY UPDATE

Our first quarter financial performance was very unsatisfactory on the two most important metrics we track.

We did not grow equity book value per unit (the increase in NBH’s equity value, which is assets minus liabilities, divided by the number of outstanding NBH membership units). We also did not achieve our targeted return on invested capital objective (NBH’s earnings adjusted for interest expense divided by the total value of equity and debt capital used in the business). As a frame of reference, NBH’s -20% growth in equity book value per unit during the quarter compares unfavorably to the S&P 500 Index’s 8% quarterly return. Additionally, our annualized -34% return on invested capital during the first quarter does not compare favorably to our 20% objective and the S&P 500 Index aggregate return on invested capital of 10%.

The primary driver of the insufficient result was worse-than-expected quarterly operating performance from S&S Filter, our largest private operating company (see the Private Operating Company Update section below for further detail). Please note a weak quarter from any of our operating companies affects the overall holding company in two ways. First, operating income from the owned private companies is considered NBH revenue, so NBH’s operating results go down when it goes down. Additionally, when an operating company loses money in a quarter, the private operating company’s carrying value on our balance sheet is reduced, i.e., an unrealized loss for the quarter (see last quarter’s letter for a more detailed discussion on this topic).

Similar to our counsel on focusing on the long-term performance of our public company collection, we don’t pay much attention to our performance over short periods. Given how our “mark-to-market” valuation accounting policy and procedure works, our overall performance can and will be volatile. Nevertheless, we fully believe we will add material value and outperform over long periods.

Our equity book value per unit has had 45% total growth (18% compounded annual growth) since inception (January 1st, 2021). This long-term performance compares favorably to the S&P 500 Index’s 13% total growth (6% compounded annually) since inception. It is important to note that a rough since-inception performance attribution shows equal contributions from the underlying cash operating performance of the private company collection and their aggregate unrealized gain in overall value. The public company collection had a minimal positive performance contribution, given its small relative size to our overall asset base.

Alternatively, a more straightforward way (using cash flow results!) to characterize our performance since inception: your holding company received cash dividends from the private operating and public companies, equating to 60% of our aggregate purchase cost of those companies

Finally, the above comparisons to the S&P 500 Index are somewhat forced: our asset collection is primarily small private companies with a small allocation to public companies vs. the S&P 500 Index comprised of large public companies. But, on the other hand, you choose how to allocate your capital, and the S&P 500 Index, as an investment option, could be considered your most practical and best alternative. Therefore, we continue to believe we will be the better option over the long term.

PRIVATE OPERATING COMPANY UPDATE

Guided by North Beach Chief Executive Officer Mike Foran and Chief of Staff Nikki Salas, our outstanding employees once again delivered excellent customer service throughout the quarter. We are grateful for their dedication and amazed at their daily ability to do what they do day in and day out. Three of our four private operating companies had a good quarter in terms of profitability and free cash flow. More importantly, business momentum and culture are improving at all four companies. At the same time, we navigate a tricky macroeconomic environment (e.g., inflation and slowing pockets of business activity here and there).

ACN Solutions

Spencer Wirick, ACN’s President, and his team continue to execute a consistent playbook of price increases, cost cuts, and marketing investments with decent returns. As a result, ACN delivered another record quarter, growing revenue by 30% and free cash flow by 40%. The simple plan for the immediate future is more of the same. At some point - of course - the benefit from past price increases runs out, leaving the power of the marketing machine. Stay tuned.

Brahler’s Cleaning & Restoration

For the third quarter in a row, Brahler’s President, Stacy Ignacio, capitalized on several big mitigation jobs (this time, it was a bunch of fires and water losses) along with our steady mold mitigation and cleaning businesses to grow free cash flow. Once again, her team exemplified everything that makes North Beach fantastic: superb execution, teamwork, and positive attitudes in the face of adversity to deliver outstanding service to our clients facing challenging situations.

Hart’s Ambulette

Hart’s President, Kristy Summers, followed a record quarter in free cash flow last quarter with yet another record quarter in free cash flow driven by high teens revenue growth. As a reminder, this results from the most significant business model change in the company’s history. As the premier service provider in its local economy, the company drastically reduced its lower-profit trips and now focuses on higher-profit trips after raising prices. Kristy’s successful effort to maintain a daily presence in key areas and add new, more profitable trip broker accounts is also working. One negative consequence of the move from lower-profit trips, which Medicaid mostly efficiently and quickly pays, is our accounts receivable are higher and older. While Kristy believes our working capital cycle will be slower going forward, she is optimistic there is room for improvement.

S&S Filter

Do you want the good news or the bad news first?

Okay - the bad news is S&S delivered its worst quarter under our ownership. The year’s first quarter is traditionally seasonally slower for our water plant and landfill end markets. We usually fill in the downtime with local industrial service work. Unfortunately, all three customer types were much slower than expected. Some of this slowdown was just customer project timing (water plants and landfills), and some of it - we believe - is macroeconomic-related, i.e., industrial customers pulled in spending to conserve cash. The good news on the bad news is the second quarter is off to a fantastic start, and our team’s morale was strong through this challenging period.

On the good news front, in March, we hired an incredible new president, James Baird, to lead S&S in its next growth phase. Most importantly, James is aligned with our core values and operating principles and believes a great culture can be a massive competitive advantage. He also brings elevated and enlightened leadership, sales & marketing skills, operational excellence, and valuable experience to our organization. In addition, he has hit the ground running, getting himself familiar with our company’s capabilities and customers and, most importantly, making great connections with our employees.

New Private Company Pipeline

Dillon Thompson, our lead man on all things private companies, focuses 100% of his time and energy on finding extraordinary, enduringly profitable, niche service companies for us to potentially purchase.

Today the top three “Power Ranking” in his pipeline are as follows:

(1) A landfill compliance service company; this is an industry we have some expertise in given our experience with S&S Filter (one of their primary end-markets is servicing the biogas filters landfill operators use to recover renewable natural gas); however, it would not be an add-on company for S&S’s biogas segment.

(2) A fuel management company that services emergency backup power systems using proprietary and technologically advanced fuel testing and reconditioning processes.

(3) An environmental service company providing consulting, operational, and laboratory services to the potable drinking water and wastewater industries.

Unsurprisingly, all the companies mentioned above adhere to our checklist: they provide essential niche services, have high recurring revenue, and are divorced from the economic cycle.

While we are not yet in the “Letter of Intent to Purchase” phase for any of them and thoroughly understand the very low base rate of successful acquisitions, we remain excited to learn from these incredibly talented entrepreneurs. They built unique businesses and are now looking for proper transition plans and suitable homes for their companies. We hope to help them.

Keen readers - I know you are - may recall our last quarter Power Ranking, which had an add-on industrial service company for S&S Filter in the top spot and a grant and loan management software and service company ranked third. The former was killed due to our inability to find a mutually agreed-upon deal structure with the seller. The latter was killed due to a sharp difference in valuation with the seller during the quarter.

PUBLIC COMPANY INVESTMENT UPDATE

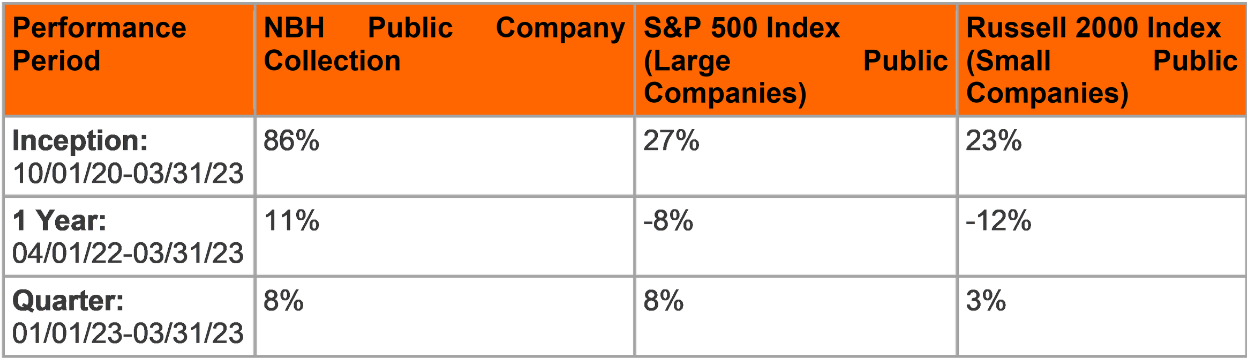

The return on the capital deployed into our public company collection compares favorably to standard general index benchmarks:

Performance

Though our aggregate public company collection is up in market value over the trailing twelve months, we don’t pay much attention to our performance over short periods. And we don’t because we fully believe we will add material value to our holding company over the long term by owning public companies with the same sought-after private company attributes mentioned above, along with:

High and stable returns on invested capital;

Long-term revenue growth runways;

Impeccable balance sheets for maximum financial flexibility;

Broad insider ownership where the management teams we partner with are aligned with us on a very long-term basis;

Most importantly, the trade-off between durable competitive advantages and the price we paid for our ownership is skewed materially in our favor.

We continue to remain relatively unexcited with the aggregate public company investment opportunity set because the broad public company market valuations are still too high based on our preferred valuation metric: free cash flow yield (total dollars left over after company expenses and maintenance capital investments divided by the total enterprise value for all of the companies in the S&P 500). That said, the S&P 500 Index’s free cash flow yield has improved some compared to valuation levels since the beginning of 2022. Today’s valuation level, however, is still nowhere near the attractive valuation levels between 2008-2011 or even the depths of the pandemic sell-off in March 2020.

Call us weird, but we get really excited when public company market values go down so that we can acquire outstanding companies at great prices. We are increasing our time devoted to public company research to add new companies to our collection that may make long-term investment sense given a practical and tight circle of competence.

That said, we added one new opportunistic position to our collection at the very end of the first quarter: Vornado Realty Trust. The essential service of this real estate investment trust is leasing and servicing ultra-high-end Class A office and retail space, mainly in New York City. The office real estate sector gravely underperformed other real estate investments and the general market recently due to terrorizing worries about a permanent shift to a work-from-home employment model and rising interest rates. Like other broad sector-specific sell-offs throughout our career, investors shoot first and ask nuanced questions never. We believe it is possible that the work-from-home model has gone too far, and big companies may call employees back to the office sooner than, well, never. We also think it is likely interest rates may not go up forever. In the meantime, we own beautiful, conservatively financed NYC real estate substantially below replacement cost with an extreme margin of safety led by a competent and rational management team with sizable insider ownership.

Other than our positions in AmerisourceBergen Corp, Berkshire Hathaway Inc., Criteo S.A., Graham Holdings Company, and Vornado Realty Trust, we will refrain from publicly identifying the other eight companies in our collection since we may add to our positions at any time. These are all illiquid, “trade-by-appointment” situations in very small public companies.

…

Despite our triumphs and challenges this quarter, we plan to continue to come to work in the spirit of Sturt’s craftspeople every day to craft three things: (1) improve our investment and operating processes; (2) improve our culture; (3) grow the equity book value per unit of North Beach all day, every day, in any way possible. We will push hard on our investment strategy’s self-sustaining flywheel, which is simply owning enduringly profitable companies that generate free cash flow that we will use to own more and more enduringly profitable companies that generate more and more free cash flow. This effort is our purpose and our indomitable will.

As always, thank you for your continued ownership of North Beach Holdings.

Best regards,

Russell P. Moenich

Investment Analyst & Executive Chairman, North Beach Holdings

President & Chief Investment Officer, RPM Capital LLC (North Beach Holdings LLC’s Managing Member)

Disclaimer:

The views expressed represent the opinion of RPM Capital LLC (RPM) and North Beach Holdings LLC (NBH). The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment.

Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While RPM and NBH believe the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and RPM’s or NBH’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance, or events may differ materially from those expressed or implied in such statements.

Forward-Looking Statements:

Certain statements in this communication constitute “forward-looking statements” within the meaning of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended (the “Acts”). Any statements contained herein that are not statements of historical fact are deemed to be forward-looking statements. The forward-looking statements in this presentation are based on current beliefs, estimates, and assumptions concerning the operations, future results, and prospects of RPM, NBH and its operating companies. As actual operations and results may materially differ from those assumed in forward-looking statements, there is no assurance that forward-looking statements will prove to be accurate. Forward-looking statements are subject to the safe harbors created in the Acts.

There are a number of important factors that could cause our results to differ materially from those indicated by such forward-looking statements, including, among other factors, risks inherent in private equity investments, competitive markets for investment opportunities, no assurance of profit or distributions, illiquidity of investments, economic and market risk, inflation and interest rate risk,lack of liquidity, lack of diversification, and conflicts of interest.

RPM and NBH undertakes no obligation to update publicly any forward-looking statements, whether as a result of new information or future events.

Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results.

This letter does not contain all the information that is material to a prospective investor.

Not an Offer – The information set forth in this letter is being made available to generally describe our investment outlook and process. The letter does not constitute an offer, solicitation, or recommendation to sell or an offer to buy any securities, investment products, or investment advisory services. Offers are made only to accredited investors by a confidential offering memorandum and related offering materials, which will contain important disclosures regarding the terms and risks of investment, and in accordance with the terms of all applicable securities and other laws. To obtain further information, including a confidential offering memorandum, you must complete our investor questionnaire and meet the suitability standards required by law. The information published and the opinions expressed herein are provided for informational purposes only.

Not Advice – Nothing contained herein constitutes financial, legal, tax, or other advice. RPM makes no representation that the information and opinions expressed herein are accurate, complete, or current. The information contained herein is current as of the date hereof but may become outdated or change.

Risks – An investment in NBH is speculative due to a variety of risks and considerations as detailed in the Confidential Private Placement Memorandum dated April 2022, and this letter is qualified in its entirety by the more complete information contained therein and in the related subscription materials.

No Recommendation – The mention of or reference to specific companies, strategies, or instruments in this letter should not be interpreted as a recommendation or opinion that you should make any purchase or sale or participate in any transaction.